Both credit cards and personal loans are examples of financial instruments that people might use to make purchases or control their spending. On the other hand, their structure, usage, and payback varied significantly.

Personal Loan:

- A personal loan is a one-time payment made to a bank, credit union, or internet lender, it often has a fixed interest rate and a certain amount of time to pay it back. These loans are perfect for larger needs like home improvements, medical bills, or reducing debt because they usually possess greater borrowing limits than credit cards.

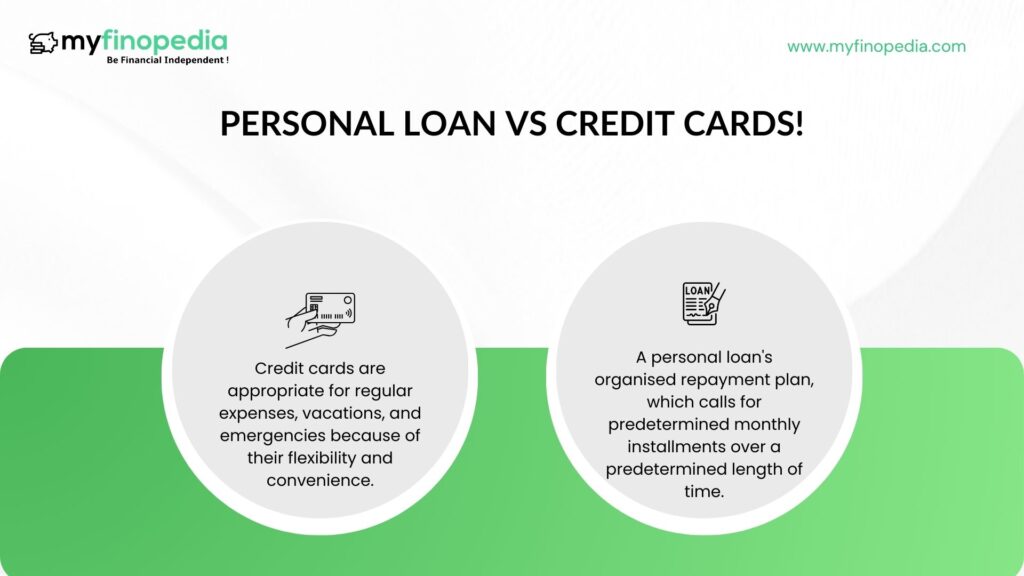

- A personal loan’s organised repayment plan, which calls for predetermined monthly installments over a predetermined length of time, is one of its key benefits. This can assist borrowers in creating more sensible budgets and warding against the temptation to make little payments, which can lengthen the repayment period and result in higher interest rates.

- Furthermore, especially for customers with high credit ratings, personal loans can have cheaper interest rates than credit cards. Over the course of the loan, this may save a sizable amount on interest costs.

- But getting a personal loan normally means paying for a credit check and sometimes even paying origination fees or other up-front expenses. A personal loan’s approval is contingent upon a number of factors, including income, debt-to-income ratio, and credit history.

Credit Cards:

- In contrast, credit cards offer a revolving credit line that enables users to make purchases up to a pre-established credit limit. Credit cards, in contrast to personal loans, have no set payback period and require minimum payments each month depending on the amount owed.

- Credit cards are appropriate for regular expenses, vacations, and emergencies because of their flexibility and convenience. Additionally, they frequently provide cashback incentives, rewards plans, and other benefits that can add value for cardholders.

- However, compared to personal loans, credit cards typically offer higher interest rates, particularly for customers who carry balances from month to month. If the debt is not paid off in full each month, there may be substantial interest charges.

In conclusion, credit cards and personal loans have diverse uses as well as particular benefits and drawbacks. While credit cards provide flexibility and convenience for regular spending, they may have higher interest rates and create the possibility of debt buildup if not used responsibly. Personal loans, on the other hand, are best for larger, one-time costs and have a defined repayment plan. Furthermore, if credit card debt is not managed appropriately, it can quickly get out of control, resulting in stress on the finances and long-term effects on credit ratings.